Suppose you start a bank with $1,000,000 in capital, and have a 10% reserve requirement. You raise that capital at the short term market rate of 1% interest and you loan out the $900,000 that you are allowed to at 4% interest for 30 year mortgages. You’re bank is set to make 3% interest on $900,000 or $27,000 a year which then goes to paying for your tellers, security guards, property tax, and live goats that the bank president sacrifices to Moloch every third full moon to prevent defaults. Whatever is left is your profit, and since I am pulling numbers out of my ass lets say profit rates at this level are 1%.

What happens if short term rates rise to 2% in your second year? I’ll tell you what happens, you aren’t making money anymore, you are in fact just breaking even. If interest rates rise above 2% then you are losing money and will be bankrupt as soon as those losses eat up the $9,000 in profits you booked the first year. How can you survive? Well if long term rates also go up by a percentage point to 5% you can raise more capital at 2% and lend it out at 5%. Your average profit margins will be smaller in percentage terms but they will be positive instead of zero or negative and your absolute profit will be higher if you can raise more than another million.

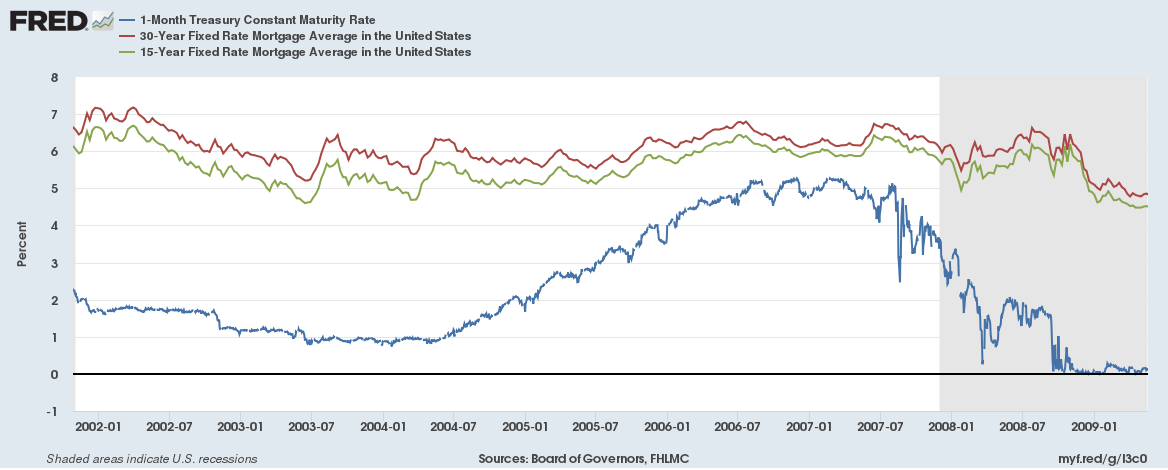

What if long term interest rates don’t lift off with the increase in short term rates? Well you could cut costs or try to increase earnings by betting on riskier investments. Or you could do both, you encourage your loan originators to pump out large numbers of loans and let them cut the quality of the loan recipient to do so. So you have guessed it, I am talking about the housing bubble again. Lets look at short term rates vs long term mortgages shall we?

OK, well 1 month Treasury rates went way up without 15 or 30 year mortgage rates really reacting but perhaps banks borrowing was cheaper?

Crap, you could get over 5% on a 3 month CD? What time to be alive… well unless you were a banker. I guess if you were a banker you could borrow from the Fed at low rates until things calmed down, right?

Well crap.

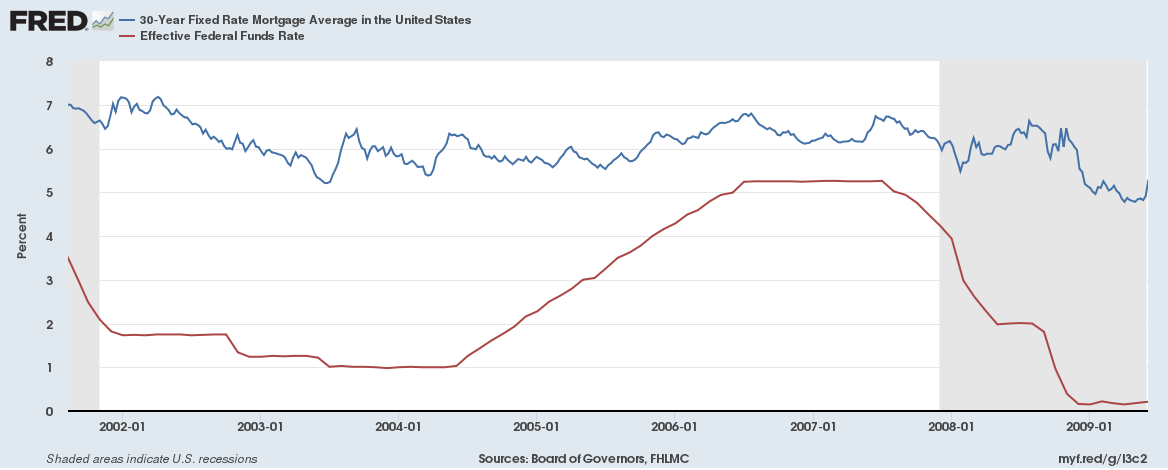

How could this happen though? How could long term rates stay so unfazed when short term rates increased by over 500% in less than 3 years? One partial explanation is that once rates start rising the attempt to maintain profitability means pumping more and more mortgages out the door from your staff (or just an increase in the dollar value of the average loan), basically “increasing” their productivity, and also increasing revenue from the loan origination costs. To loan more however you have to raise more capital so all the banks are competing to draw in more dollars to loan out quickly. You also have to convince people to take the loans out, which means ferocious competition on the mortgage side keeping those rates down.

This doesn’t explain everything, such as why the short term rates increased in the first place, but it fits with a lot of what happened from 2004 through 2008. The effect will be larger or smaller based on the total amount of loans made before the rates started to rise, the larger the amount the more stress on the system. How are things going now?

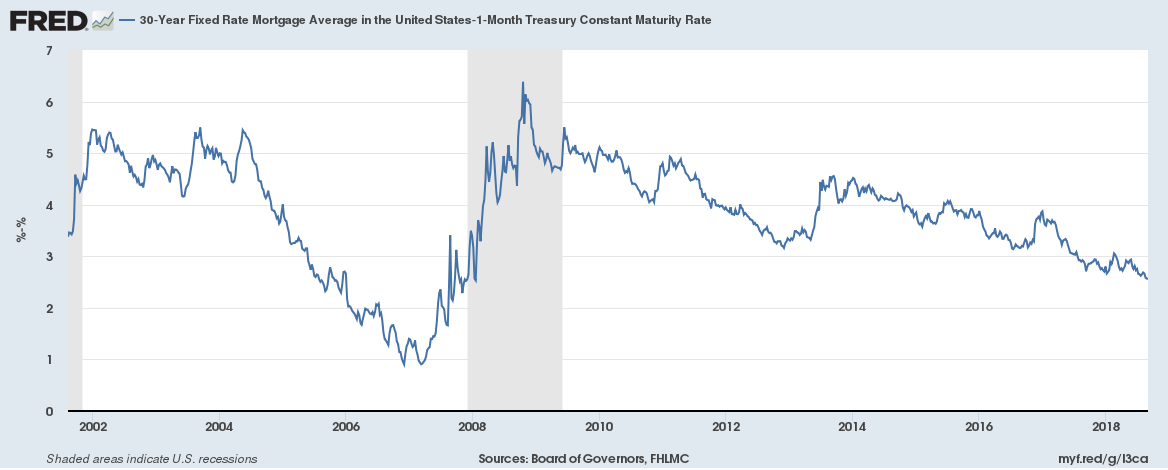

The spread is definitely compressing, here is the 30 year mortgage minus the 1 month Treasury rate

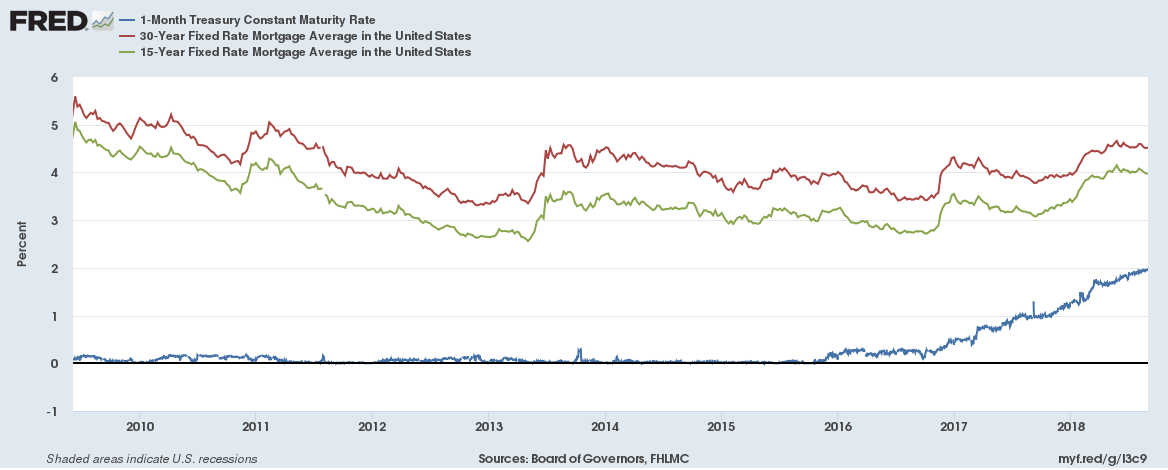

But don’t expect banks to make the exact same mistake twice, it is unlikely that there will be a massive surge in subprime lending this time around. Honestly they aren’t even being pressured to thanks to the Fed’s interest on reserves (IOR) program, which has had its rate pushed up to almost 2% and has basically kept pace with short term borrowing costs allowing banks to carry large amounts of reserves essentially for free recently.

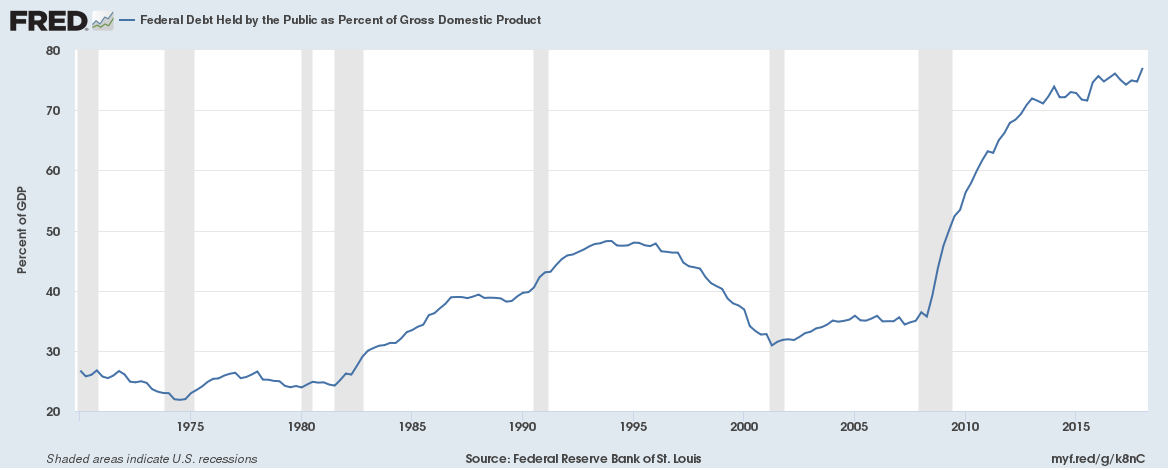

The growth in debt that has been driving interest rate increases recently has been government issued.

There are three things that are particularly insane about this graph. First that the economy has been at or above full employment and debt to GDP is still increasing (albeit at a much slower rate than from 2008 through 2013), and secondly interest rates have been extremely low pushing the cost of borrowing down for the government and reducing one of its major costs. Thirdly the Federal reserve has been remitting roughly 60 billion dollars more per year post crash than it did pre crash thanks to its earnings.

The sum of these three is significant. The 2001 recession saw tax revenue drop by about 1.5% of GDP and it took until 2005 to exceed revenue from the year 2000 (partly due to tax cuts), the 2008 recession saw revenue drop by about 2.5% of GDP and did not see its 2007 peak exceeded until 2013. A simplistic projection assuming tax receipts in 2007 staying stable vs dropping implies that the crash added 1.2 trillion dollars to the debt due to lower tax receipts alone. This would be more if you compared to the average growth rate of receipts leading into this era. Meanwhile the Fed has remitted around 600 billion dollars more to the Federal government over the last 10 years more than the trend leading into the Great Recession, and interest rates on government debt have been extremely low, had they been merely low (2 percentage points higher) with the same spending+tax rates then debt would be around 2 trillion dollars higher.

The fact that Federal debt levels have risen as a percentage of GDP over the past two years with these tailwinds is concerning, but there are a few points preventing things from getting out of control immediately. First is that only about 60% of the Federal debt comes due in the next 4 years, which means that an interest rate hike of 1 percentage point right now would increase annual debt payments by less than 25 billion (assuming an even distribution of maturing debt over the next 4 years) in the first year, and of around 90 billion by the end of the 4th year.

The second major point is that during a recession the Fed typically ‘stimulates’ by slashing interest rates and increasing its balance sheet which increases remittances, meaning that the Federal government is unlikely to have to fact the trifecta of rising interest rates, lower remittances and lower tax revenues all together.

To be continued.

No comments:

Post a Comment