An inverted yield curve means smaller net interest margins for financial firms and thus less financial intermediation. That is, once the yield curve inverts, it goes from being a predictive tool to a causal agent.

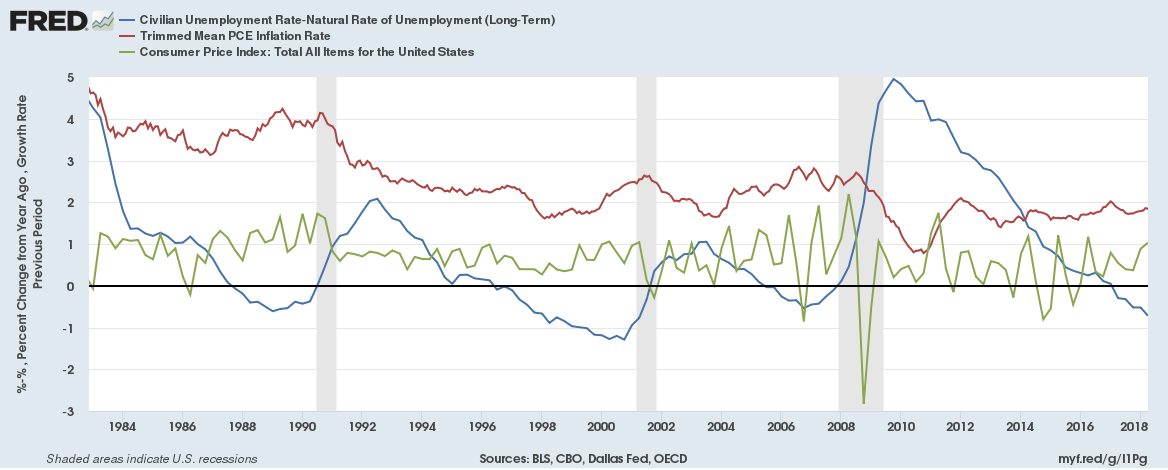

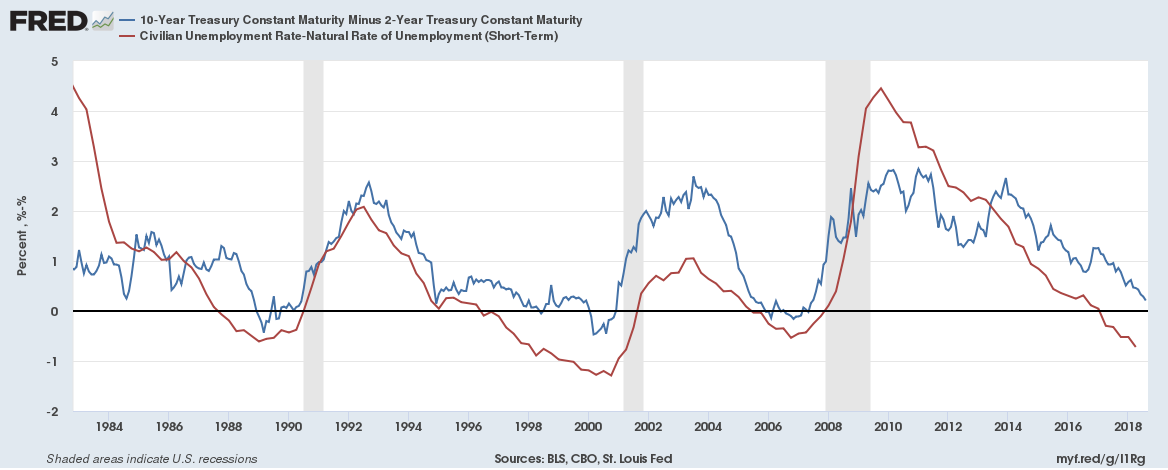

There is a problem with this statement, it is hard to square with the actual economic outcomes. For example the UE rate tends to drop or remain at low levels while the yield curve is inverted (UE rate is divided by 2 in these graphs to make it easier on the eyes).

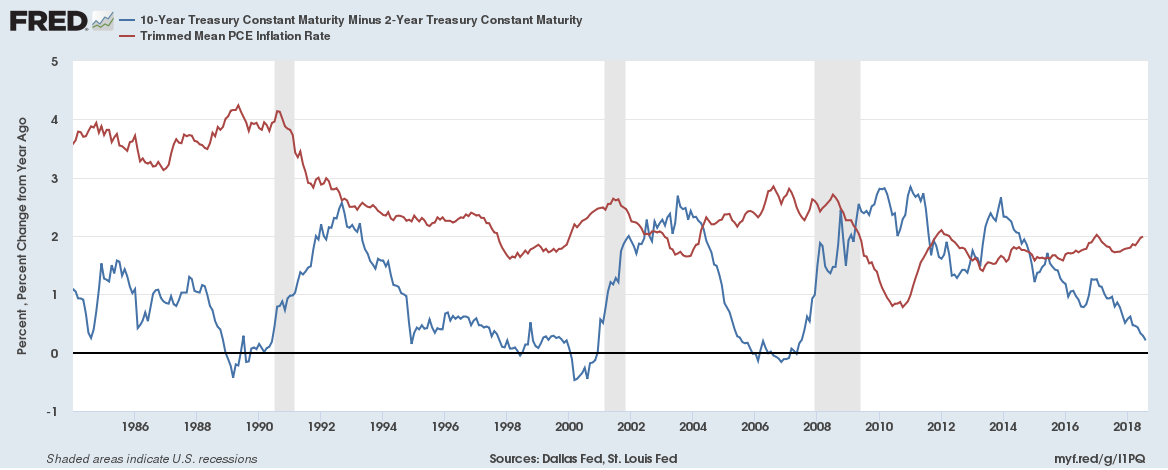

The 2000 recession

And the early 1990s recession

Nor does the market show fears of a recession

If we look at mortgage originations by quarter or by year it is not obvious that the curve inversion of late 2005/early 2006 resulted in diminished financial activity, nor that the flattening yield curve in 2005 led to diminished financial activity (there is no reason to believe that an inverted yield curve reduces earnings significantly more than a flattened yield curve). By year, for the 2000s, the highest origination amounts were 2003, 2005, 2006, 2004, 2002, 2007, 2009, 2001, 2008, 2000. The largest yield curve spread was in 2004 and the smallest was 2006/2007.

So, looking at the Great Recession it appears that UE decreased, markets increased and mortgage originations stayed at high levels (certainly didn't decline) and the curve was inverted for most of 2006 through June 2007 which puts some counters out of the question (such as indicators lagging by several quarters unless by several quarters meaning 6+).

So what is going on?

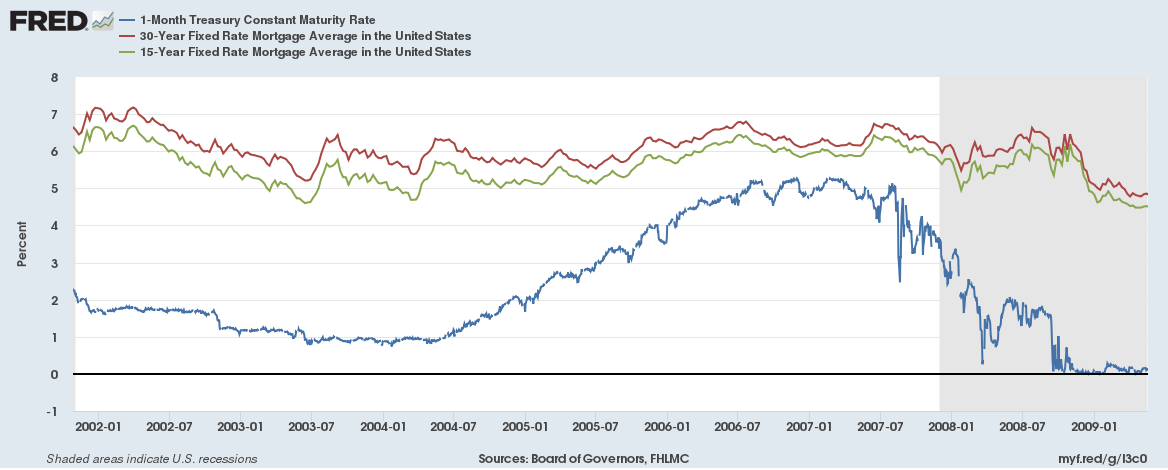

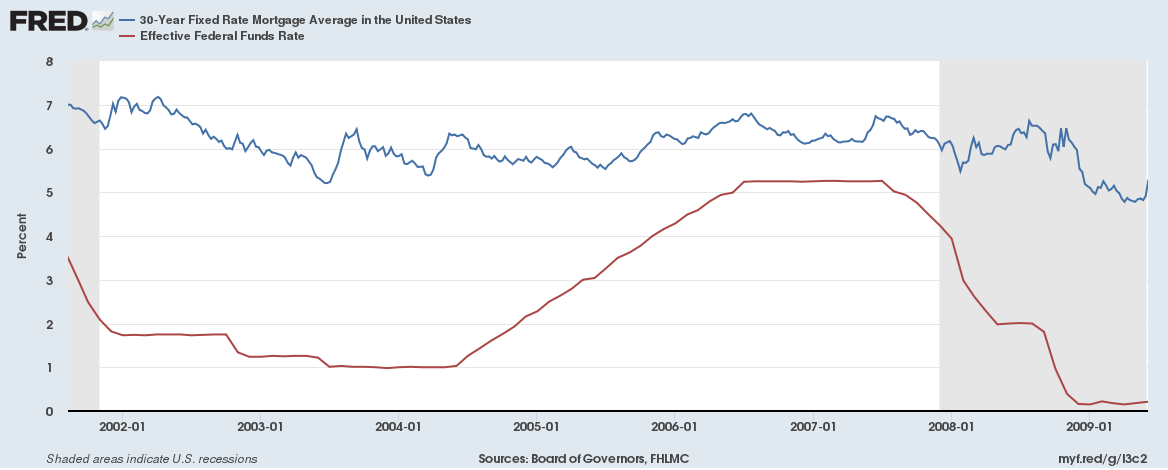

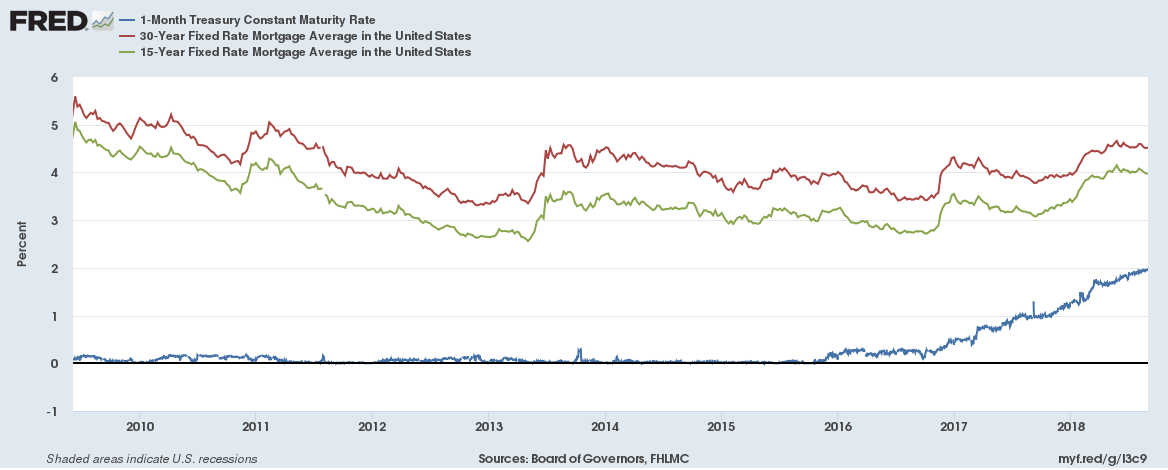

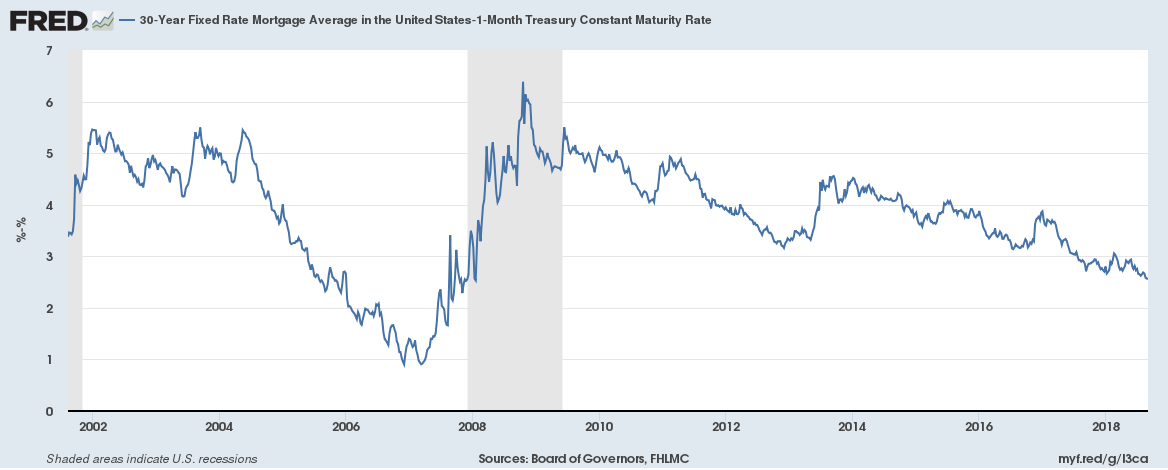

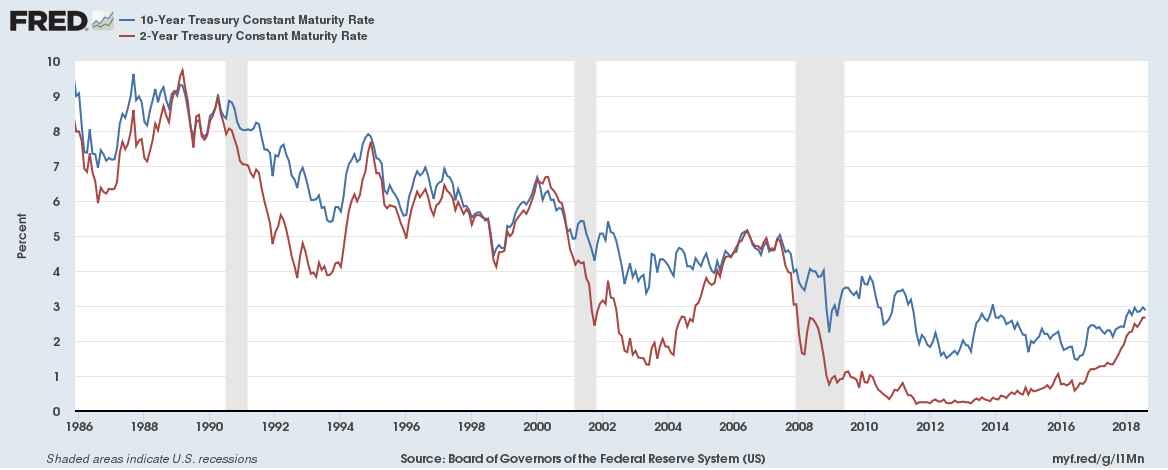

With all the discussion about yield curve inversions almost no one bothers to mention the obvious fact that they are stupid. They shouldn't happen. Why would you lend someone money at 2% interest for 10 years when you could lend that same person money at 2.1% interest for 2 years? It takes some very convoluted situations to come up with plausible reasons. I am happy to say though that it is hard to find market based curve inversions. The 30 year mortgage rate doesn't dip below the 15 year rate as far back as FRED data goes and neither of the 30 year mortgage or 15 year mortgage ever dips below the overnight or 3 month interbank rates. However the 30 year treasury does, meaning it isn't simply an artifact of a longer term on the high end.

So yields invert when Fed influenced rates climb without market influenced rates climbing an equivalent amount, eventually, after multiple rate hikes, the short end pops over the long end, but again only on securities that are influenced by the Fed, and we see no overt, short term signs of broad economic trouble.

This means that there must be, somewhere, large frictions in the financial markets. Why? Well investors are trying to make money, if short term rates are rising relative to long term rates then people who lend at long term rates should move into at least some lending at short terms, and some people borrowing at short terms should prefer to borrow at long terms now. These are strong pressures and they should be somewhat proportional to the size of rate changes.

Basically people (or institutions) who are happy to lend long aren't interested in lending short, and people who borrow short aren't interested in borrowing long. Shouldn't an increase in short rates hit the market somehow though? People who borrow short should see higher costs and reducing their borrowing which should filter out to the market. Well there are basically three options that you have when a strategy isn't working, switch to an alternate method, pull out entirely and double down on the current one. Clearly switching to alternate methods of funding hasn't been happening or the curve wouldn't narrow and then invert, pulling out appears not have happened after recent inversions leaving us with doubling down.

What would this look like? If you are going to pay more for financing without a rise in long term profitability (ie flat long term rates) then you are going to need to add risk to boost earnings. There are a lot of reasons why such a course might sound sensible, you expect short term rates to come back down and are just trying to weather the storm, or your compensation is strongly tied to the upside and only weakly to the down side, or any other number of situations.

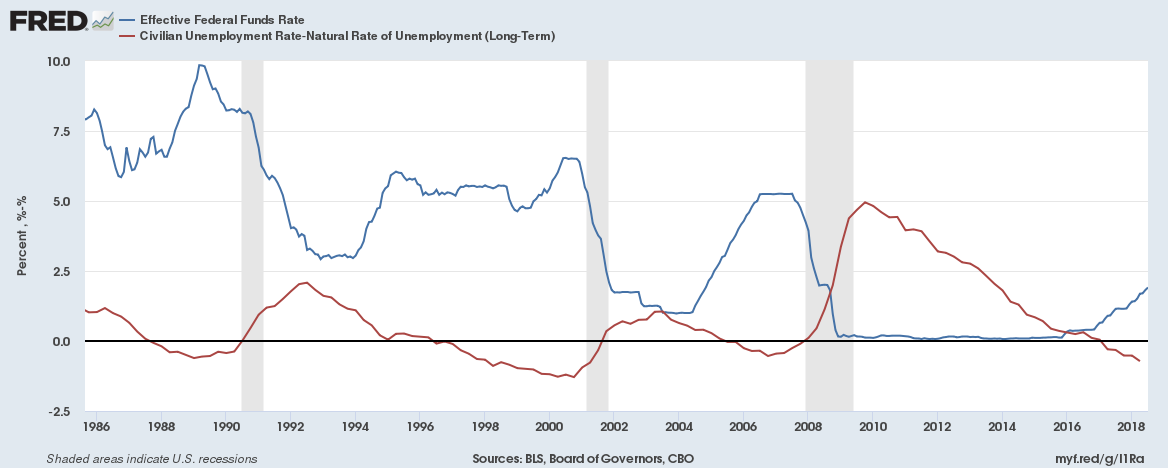

This expectation fits very well with what we saw in 2005 through 2007, subprime loans (representing higher risk) almost doubled as a share of the market and increased by nearly 5 times in total dollars from the late 90s. Adjustable rate mortgages (ARMs) roughly doubled from 15% to 30% of the market as well, fitting in with our hypothesis of greater risk taking by short term borrowers (banks). This also fits the margin run up in the late 90s as the tech bubble peaked along with an inverted yield curve. We can also start to formulate an explanation for the inconvenient truth that the Federal Reserve has been lowering interest rates (ie easing) into each of the past 3 recessions, getting "ahead of the ball" by a quarter at least without being able to prevent it with stimulus as is supposedly possible.

Eventually borrowed money has to be repayed, margins have to be satisfied. The race up where you borrow to gain exposure turns into a race down where investors at first liquidate to realize gains followed by to late investors liquidating to prevent further losses, a Minksy Moment. However, instead of relying on explanations based on greed (aren't people always greedy?) or hubris (aren't they always filled with this?) we have a rational explanation. The Fed cutting rates makes the previous strategies profitable again with lower risk.