The Federal Reserve is currently planning on two related courses of action in the near future, first to continue unwinding portions of its balance sheet and secondly to steadily increase interest rates and tt is difficult to see how they could accomplish the former without the latter occurring. Unwinding the balance sheet should have a dual effect on pushing up rates, first it increases the available supply of securities as they are functionally off market, and secondly should lead to lower remittances to the treasury, increasing the deficit and increasing the supply of Treasuries.

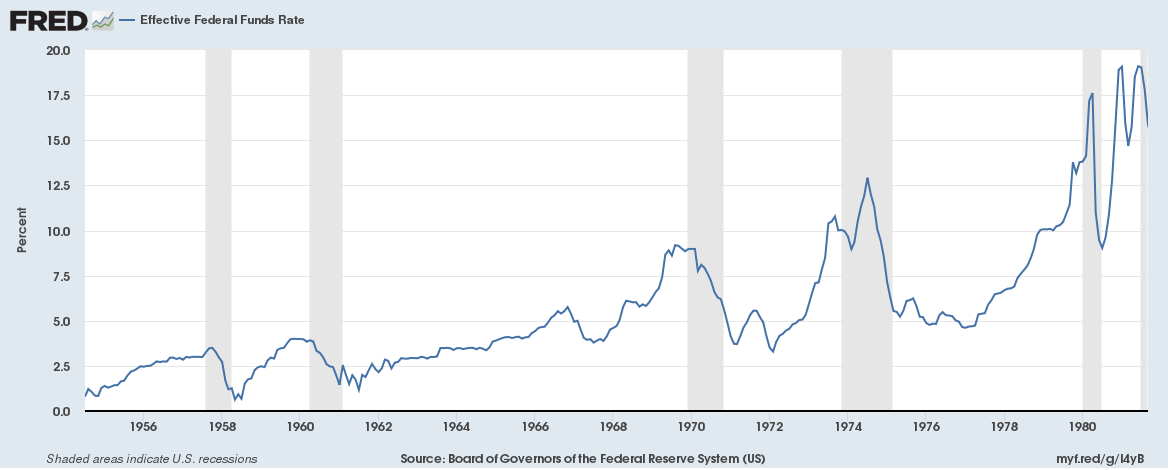

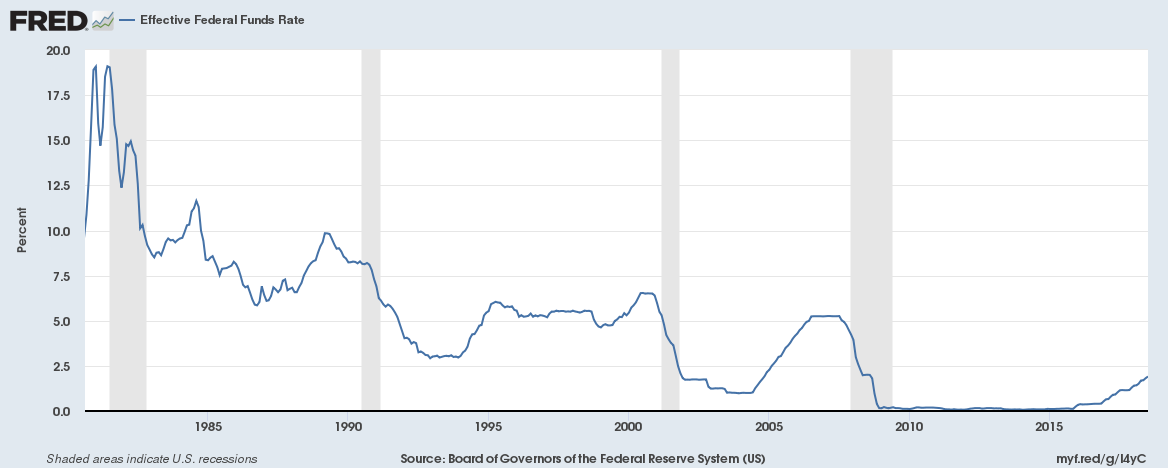

Here I am going to split the federal funds rate into two eras, 1950s through the early 1980s and the 1980s through present day

Here we have rising interest rates where almost every peak or trough is higher than the previous peak or trough up until the early 80s when we get declining interest rates where almost every peak or trough is lower than the previous peak or trough. The switch from rising to falling interest rates concurred with a dramatic shift in Fed policy. Functionally the full employment mandate was ignored for a period in the name of price stability and the funds rate was increased dramatically. As the Federal Reserve is giving no indications of a major departure from current policy I conclude that the current rising interest rate trend will be similar to the trend from the last 35+ years. Thus I expect the current rise in interest rates (as measured by the federal funds rate) to peak below the 5.25% that saw for parts of 2006 and 2007. My best guess is that it will peak under 4%, but my investment decisions will not hinge on this guess, merely be optimized somewhat in favor of it.

While Treasury rates should follow the direction of the federal funds rate there is a good chance that shortish term Treasuries will rise somewhat faster, in fact to an extent they already have.

Here we see that 1 and 2 year Treasury rates have increased by about 25% more than the funds rates since 2013 . We can also see that this happened around 1993 and 1999. That the Fed intends to wind down their balance sheet in the near term increases the chance that short term Treasury rates will rise faster than the funds rate.

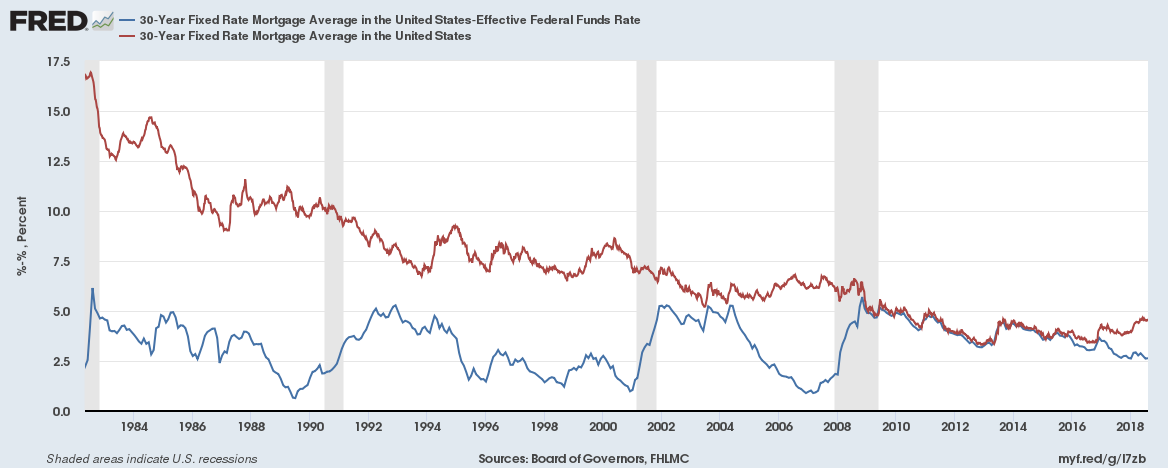

Here I want to revist something I have mentioned a few times, but in more detail, that the rises in short term interest rates aren’t pushing up long term interest rates.

The Blue line is the spread between the 30 year mortgage and the federal funds rate, and the red line is the 30 year mortgage rate. Remember that the low points for the blue lines are when the spread is very small, and you can see that the spread decreases dramatically several times without much (or any) push up or down in long term rates. As long as this pattern holds (and it isn’t guaranteed as this is not the pre 1980s pattern) this should mean that short term rates peak at under 5%, and probably under 4.5%, before the Fed starts cutting into the next recession.

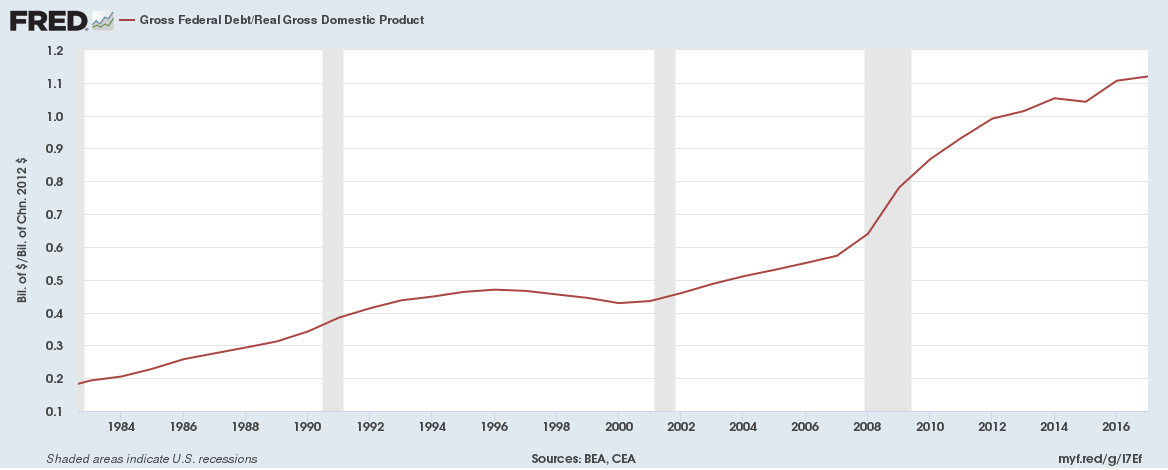

This is the good news for government debt, the rise in interest rates shouldn’t become a rocket and the duration won’t be for so long that all government debt feels the rise. On the other hand the federal government has been getting less good about piling on debt.

And a shift in long term rates

And a shift in long term rates WHAT

ReplyDelete