No real demand spike, but a persistent decline in excess reserves has been decreasing the available supply.

It seems unlikely that there is no maximum level of debt for a country, be it government, private or combined. Obviously it would be shifting based on factors such as interest rates but conceptually it is hard to argue that debt to gdp ratios can go up indefinitely, and it is likely an empirical answer you will get.

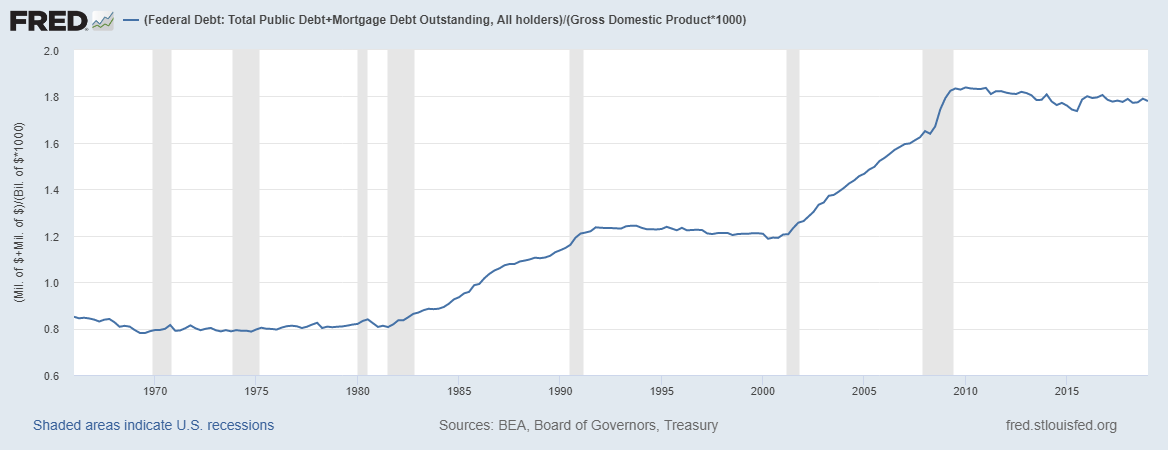

So here we are, a major financial crisis that started with massive debt levels and 10 years later those levels are roughly the same. We have now a strong policy of government stimulus in the face of recessions, with 2008 starting with a little remembered 110 billion dollar stimulus before a recession was officially recognized which came 7 months after the Fed started an easing cycle. Who is going to get hit this time if debt is increased?

To maintain the current level of total debt there will have to be a reduction to offset any government stimulus. The price rise you see above should be viewed even more skeptically than the one up until 2007 because it is on lower volume. Below is existing home sales (had to change sources)

Plus new home sales

We are looking at significantly lower volume, significantly less dollar value to gdp for mortgages in a larger country (in real prices the peak isn't as high as the previous peak though).

If this next recession is significant, with significant additional government debt I would expect home sales volume to die, and when volume dies volatility explodes.

No comments:

Post a Comment