Now money is fairly unique as a medium of account. Within a currency zone, say the US, the national currency does the majority of the heavy lifting (yes exceptions exist) when it comes to transactions.

On the other hand there are many competitors for stores of value, and I am not just talking about gold. Stocks, bond, and precious metals can all, under the right circumstances, be vehicles for storing and increasing wealth. The closer to zero that interest rates drop the less of a distinction there is between cash and other "stores of value". This is all basic, generally accepted, stuff.

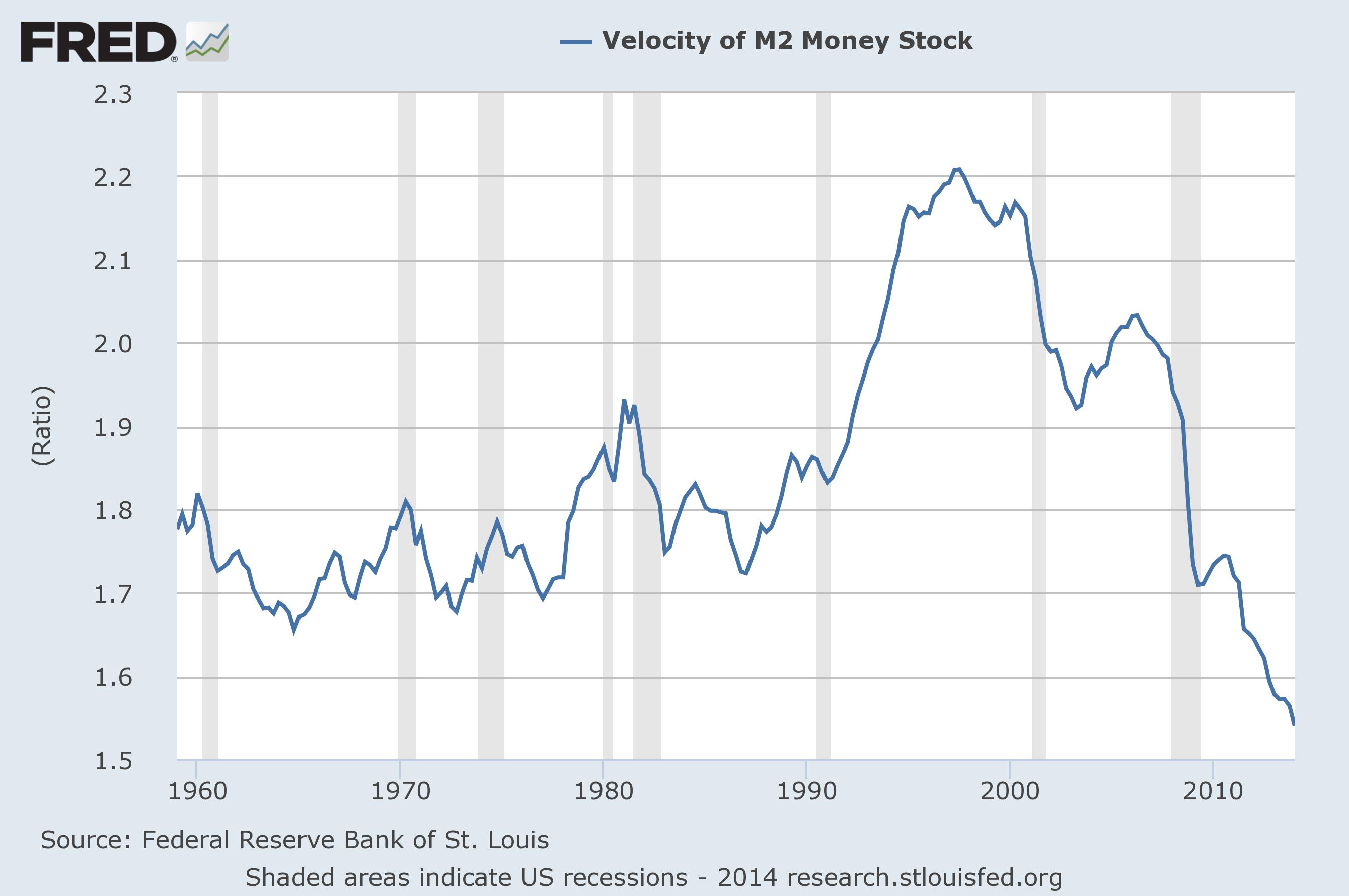

So the question is how does QE work? When a CB prints and swaps out dollars for bonds- be they government or private- they are swapping one store of value for another. If there was a shortage of cash and people wanted to make purchases but were cash (or liquidity) constrained then you could make a case that by swapping cash for bonds provides a functional value to the economy and that money will move around. But what evidence is there for a lack of cash in the system? M2 velocity has been declining since the late 90s-

These are really pretty basic ideas in economics I know, but they fundamentally explain how the ECB can promise to buy AT LEAST 1 trillion Euros worth of bonds and nudge expected inflation around 0.2%.

OK- back to what I said about stores of value- I mentioned PMs, but funnily enough there really isn't any evidence of them being a store of value since the US dollar went off the gold standard in 1913 (haha!) it has been highly volatile and it is not at all appropriate to call PMs a store of value. So what? Well if gold isn't a store of value, and gold isn't used as a medium of account then central banks can force inflation buy buying gold.*

The irony here is delicious on all sides. If central banks started buying gold to push inflation they would be making it more and more like a store of value, making it more like money, after decades of fighting to make it less like money. On the other hand gold bugs (in recovery myself) look at purchases of gold by central banks and say "look at Russia/China buying gold" they are going to create a stronger currency that can someday compete with the US dollar.

*Why gold and not something else? Anything else would do (like oil, wheat or silver) but those things are either far less practical to store or are used heavily in industry or both. Purchasing them in large amounts would not only drive up prices but also limit supply which would cause negative shocks to the economy.

No comments:

Post a Comment